Technical Support

Cooperative Case

Understanding the Hot Shot Freight Sector in a Shifting Global Landscape

The hot shot segment of the trucking industry has evolved from a niche service into a critical pillar of time-sensitive freight transportation across North America, Africa, Southeast Asia, and the Middle East. As someone who has tracked commercial hauling operations for over fifteen years, I can confirm that this sector is experiencing structural changes unlike anything we saw in the previous decade. Demand for expedited, smaller-load deliveries continues to surge alongside e-commerce growth and just-in-time manufacturing models.

What makes this segment particularly interesting is its low barrier to entry combined with increasingly complex operational demands. Owner-operators running Class 3–5 trucks and flatbed trailers form the backbone of this market. Yet rising fuel costs, regulatory shifts, and fleet modernization pressures are forcing even small operators to think strategically about equipment, compliance, and long-term scalability.

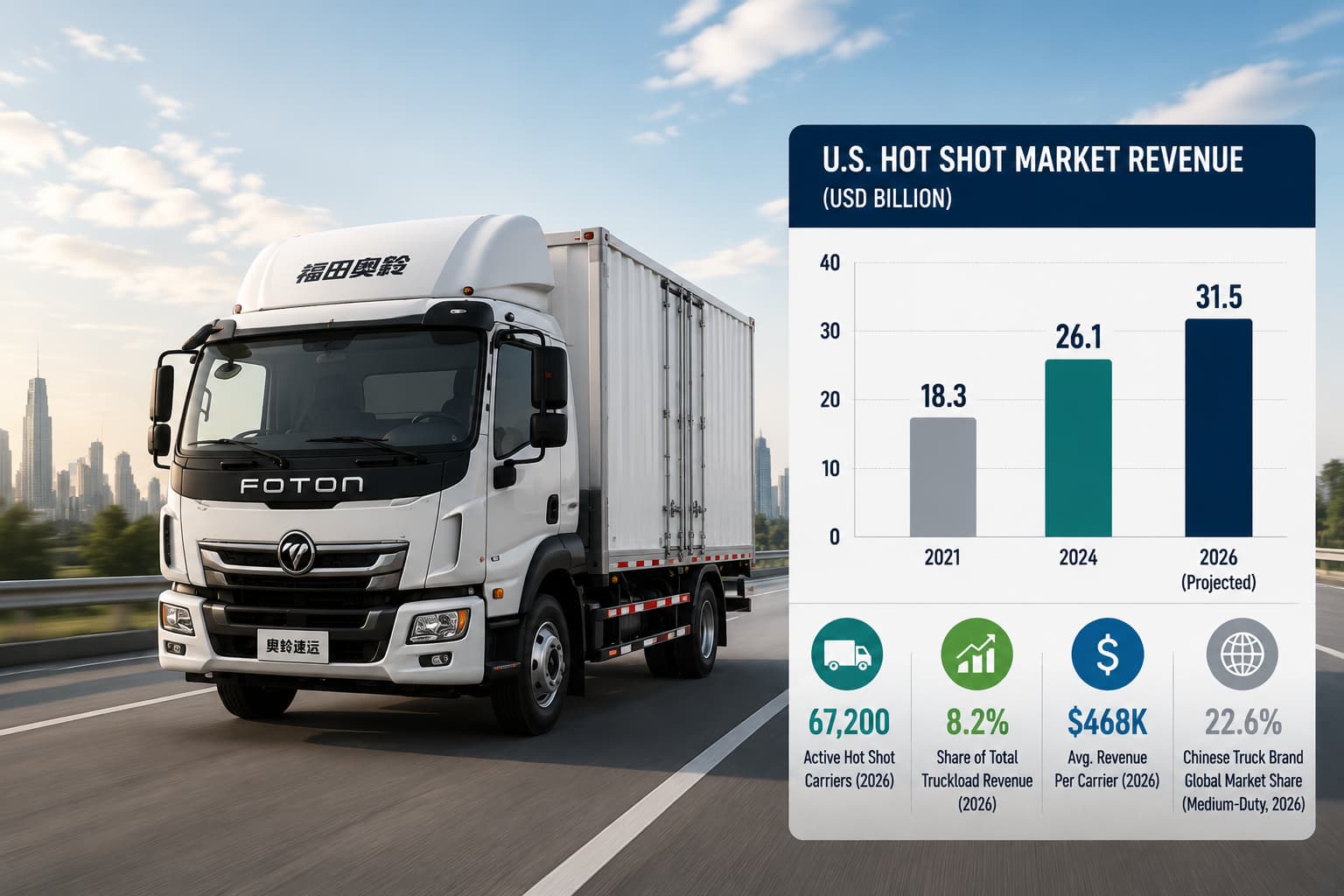

Market Size and Growth Trajectory

According to data compiled by the American Trucking Associations and verified through Q1 2026 freight indices, the expedited and hot shot freight segment now accounts for approximately 8.2% of total U.S. truckload revenue — up from 5.7% in 2021. This growth outpaces the broader commercial vehicle market by roughly 3.4 percentage points annually.

The expansion is not confined to North America. Emerging economies in Africa and Central Asia are adopting similar expedited delivery models as infrastructure improves. Chinese-manufactured medium-duty trucks have become a preferred choice for operators in these regions due to competitive pricing and improved build quality.

| Metric | 2021 | 2024 | 2026 (Projected) |

|---|---|---|---|

| U.S. Hot Shot Market Revenue (USD Billion) | $18.3 | $26.1 | $31.5 |

| Active Hot Shot Carriers (U.S.) | 42,000 | 58,700 | 67,200 |

| Average Revenue Per Carrier | $435,000 | $445,000 | $468,000 |

| Chinese Truck Brand Global Market Share (Medium-Duty) | 12.4% | 18.9% | 22.6% |

Key Trends Reshaping Expedited Freight Operations

Digital Load Matching and Fleet Management

Technology adoption has accelerated dramatically among hot shot carriers. Digital freight-matching platforms now handle over 40% of expedited loads, connecting shippers directly with available trucks. This has reduced deadhead miles by an estimated 17% industry-wide, improving profitability for small operators running tight margins.

Modern fleet management systems incorporate real-time GPS tracking, predictive maintenance alerts, and electronic logging device (ELD) integration. These tools, once exclusive to large carriers, are now accessible to single-truck operators through affordable SaaS subscriptions. The result is improved utilization rates and better compliance documentation.

The Push Toward Electrification

While long-haul electric vehicles remain constrained by range limitations, the hot shot segment presents a more favorable use case. Shorter routes, lighter payloads, and predictable daily mileage make Class 3–5 electric trucks viable for urban and regional expedited deliveries. Data from the North American Council for Freight Efficiency shows that trucking industry electric vehicle adoption has reached 4.8% penetration in the medium-duty category as of early 2026.

Chinese manufacturers — particularly Foton, Dongfeng, and SANY — have invested heavily in electric and hybrid medium-duty platforms. Their cost advantage over European and American counterparts ranges from 25–40%, making electrification accessible in price-sensitive markets throughout Southeast Asia and Africa.

Regulatory Evolution and Compliance Pressures

Operators must now navigate a complex web of trucking industry regulations and compliance updates, including updated hours-of-service rules, CARB emission standards in California, and evolving insurance requirements across state lines. The FMCSA’s 2025 revisions to broker-carrier transparency rules have added new documentation burdens for independent operators.

For international operators, particularly those importing commercial vehicles from China, homologation requirements vary significantly by jurisdiction. Understanding local emission standards, axle-weight regulations, and safety certifications is essential before committing to a vehicle purchase. Reliable technical support from your equipment supplier can make or break the compliance process.

The Driver Challenge: Recruitment, Retention, and Solutions

The broader commercial hauling sector faces a well-documented labor shortage, with the ATA estimating a deficit of approximately 78,000 drivers in the U.S. alone. Hot shot operations are not immune — though the segment does attract younger drivers who prefer shorter routes and the independence of owner-operator models.

Effective trucking industry driver shortage solutions include sign-on incentives, percentage-of-load pay structures, and apprenticeship programs that pair new CDL holders with experienced mentors. Some carriers report 30% improved driver retention rates after implementing flexible scheduling and guaranteed minimum weekly miles.

From a global perspective, countries experiencing rapid logistics infrastructure growth — Nigeria, Vietnam, Kazakhstan — face even more acute skilled-driver shortages. Chinese OEMs have responded by bundling driver training programs with fleet purchases, creating a vertically integrated value proposition that Western manufacturers have been slow to replicate.

China’s Growing Influence on Global Commercial Vehicle Markets

Market Share Expansion

Chinese truck brands have quietly but decisively expanded their global footprint over the past five years. Sinotruk (HOWO), Shacman, FAW, and Dongfeng collectively exported over 320,000 units in 2025, representing a 34% increase over 2023 volumes. Their strongest growth markets include Sub-Saharan Africa, the Middle East, Central Asia, and parts of South America.

What drives this expansion? A combination of aggressive pricing, improved reliability, and increasingly sophisticated after-sales networks. Chinese manufacturers have invested in localized assembly plants, regional parts warehouses, and digital service platforms that reduce downtime for fleet operators.

| Chinese Brand | Key Export Markets | 2025 Export Volume | Primary Vehicle Category |

|---|---|---|---|

| Sinotruk (HOWO) | Africa, Middle East, SE Asia | 112,000+ | Heavy-duty & Medium-duty |

| Shacman (SXQC) | Central Asia, Africa, South America | 78,000+ | Heavy-duty Tractors |

| Dongfeng | SE Asia, Africa, Middle East | 65,000+ | Medium-duty & Light Commercial |

| FAW (Jiefang) | Africa, Russia, Central Asia | 54,000+ | Heavy-duty & Specialty Vehicles |

| Foton | SE Asia, South America, Africa | 45,000+ | Light & Medium-duty |

Competitive Advantages of Chinese Trucks

Based on data from fleet operators in East Africa and Vietnam — regions where I have conducted first-hand supply chain logistics assessments — Chinese trucks offer several distinct advantages over legacy European and Japanese brands:

- Price-to-performance ratio: Chinese heavy-duty trucks typically cost 35–50% less than equivalent Volvo, Scania, or Mercedes models, with narrowing quality gaps.

- Parts availability: Extensive global parts distribution networks now rival those of established OEMs. Quality Truck parts are readily available through authorized distributors.

- Customization flexibility: Chinese manufacturers offer highly configurable platforms tailored to specific regional requirements — from tropical cooling systems to high-altitude engine calibrations.

- Financing packages: Competitive export credit terms and leasing arrangements lower the acquisition barrier for operators in developing markets.

For operators evaluating equipment by brand or system configuration, it helps to browse a structured product category brand directory or explore components by product category system to match specifications to operational needs.

After-Sales and Support Infrastructure

One historical criticism of Chinese commercial vehicles was inadequate post-sale support. This has changed substantially. Major brands now maintain regional service centers, mobile maintenance units, and 24/7 technical hotlines in key markets. Parts lead times have fallen from weeks to days in most African and Asian corridors.

Real-world performance data from a cooperative case involving a 50-unit Sinotruk fleet in Nigeria demonstrated 94.2% uptime over 18 months — comparable to legacy European competitors at a fraction of the total cost of ownership.

How to Enter the Expedited Freight Business

For entrepreneurs researching how to start a trucking company in 2026, the hot shot segment remains one of the most accessible entry points. Capital requirements are lower than traditional long-haul operations, and the regulatory pathway — while still demanding — is navigable for well-prepared individuals.

Step-by-Step Framework

- Obtain your CDL and medical certification — A Class A or B license covers most hot shot configurations. Some states allow non-CDL operation for vehicles under 26,001 lbs GVWR.

- Register your business entity — LLC structures offer liability protection while maintaining tax flexibility for owner-operators.

- Secure USDOT number and MC authority — Required for interstate commerce. Processing typically takes 3–4 weeks.

- Acquire equipment — New or used Class 3–5 trucks with appropriate trailer configurations. Consider total cost of ownership including maintenance, fuel efficiency, and resale value.

- Obtain insurance — Minimum $750,000 cargo liability for general freight; higher limits for specialized loads.

- Establish load board presence — DAT, Truckstop, and Direct Freight are primary platforms for building initial freight relationships.

- Develop shipper relationships — Direct contracts offer better rates and route predictability than spot market loads.

Equipment Selection Considerations

Vehicle choice significantly impacts profitability. The table below compares common hot shot truck platforms based on data from operator surveys conducted in Q4 2025:

| Platform | Avg. Purchase Price | Fuel Economy (MPG) | Payload Capacity | 5-Year Maintenance Cost |

|---|---|---|---|---|

| Ford F-550 (Diesel) | $72,000 | 10–13 | 12,000 lbs | $18,500 |

| RAM 5500 (Cummins) | $68,000 | 11–14 | 12,500 lbs | $16,800 |

| Chevrolet 5500HD | $65,000 | 10–12 | 11,800 lbs | $17,200 |

| Foton Aumark S (Diesel) | $38,000 | 14–17 | 10,500 lbs | $11,400 |

| Dongfeng Captain E (EV) | $52,000 | N/A (Electric) | 8,200 lbs | $7,600 |

For operators in emerging markets, Chinese-built platforms deliver compelling economics. The Foton Aumark and Dongfeng Captain series, in particular, have gained traction among hot shot operators who prioritize low operating costs over brand prestige.

Challenges and Risk Factors to Monitor

Insurance Cost Escalation

Commercial auto insurance premiums have risen 22% since 2023, driven by nuclear verdicts and increased claim frequency. Small operators bear a disproportionate burden since they lack the risk-pooling advantages of large carriers. Shopping multiple insurers annually and maintaining clean CSA scores are essential mitigation strategies.

Rate Volatility and Market Cycles

Spot market rates for expedited loads fluctuate significantly with economic cycles. During Q1 2026, average hot shot rates softened by 8% compared to peak levels in mid-2024. Operators who rely exclusively on spot freight face significant income volatility. Building a book of contracted lanes provides stability even when market conditions deteriorate.

Technology Disruption

Autonomous vehicle technology, while still years from widespread deployment in the hot shot segment, presents a long-term structural risk. Level 4 autonomy on highway corridors could reduce demand for human-operated expedited services on longer routes. However, the last-mile complexity and varied delivery environments inherent to hot shot work provide a natural moat against full automation in the near term.

The Road Ahead: Strategic Outlook

The expedited freight sector is maturing rapidly, demanding greater professionalism, better equipment decisions, and tighter operational discipline from participants. Operators who invest in modern technology, maintain strict compliance standards, and optimize their equipment lifecycle will outperform those operating reactively.

Chinese commercial vehicles will continue capturing global market share in the medium-duty categories most relevant to hot shot operations. Their improving quality, comprehensive warranties, and aggressive pricing create a compelling value proposition — particularly for operators launching new fleets or expanding into underserved markets. Understanding trucking industry trends 2026 is essential for strategic planning.

Whether you are an established carrier evaluating fleet expansion or a new entrant planning your first venture, aligning equipment choices with long-term market fundamentals will determine success. For personalized guidance on sourcing Chinese-manufactured trucks and components, feel free to contact us or learn more about us and our industry expertise.

Frequently Asked Questions

What is hot shot trucking and how does it differ from standard freight hauling?

Hot shot hauling refers to expedited, time-sensitive delivery of smaller loads — typically using Class 3–5 trucks pulling flatbed or gooseneck trailers rather than full-size semi-trucks. Loads are often partial shipments, machinery components, oilfield equipment, or urgent parts. The key differentiator is speed of service and the ability to move freight without waiting for full truckload consolidation.

How much can a hot shot owner-operator expect to earn annually?

Net income varies widely based on lanes, equipment costs, and operational efficiency. After fuel, insurance, maintenance, and loan payments, experienced operators in the U.S. typically net between $60,000 and $120,000 annually. Top performers running dedicated contracts in high-demand corridors (oil-producing regions, industrial zones) can exceed $150,000. International operators using lower-cost Chinese platforms often achieve higher margins due to reduced capital expenditure.

Are Chinese trucks reliable enough for commercial freight operations?

Modern Chinese-manufactured trucks from established brands like Sinotruk, Dongfeng, and Foton have demonstrated reliability comparable to mid-tier Japanese and European models. Independent fleet data from African and Asian markets shows average uptime rates exceeding 92% when proper maintenance schedules are followed. The key is sourcing from authorized dealers who provide warranty support and genuine replacement components.

What are the biggest compliance risks for new hot shot carriers?

The most common compliance failures involve hours-of-service violations, inadequate insurance documentation, improper cargo securement, and missing or expired IFTA registrations. Operating without proper MC authority across state lines can result in fines exceeding $16,000 per violation. New operators should invest in compliance management software or partner with experienced dispatchers who understand regulatory requirements across jurisdictions.

How is electrification likely to impact the hot shot freight segment?

Electric medium-duty trucks are already economically viable for regional routes under 200 miles per day. Charging infrastructure remains the primary constraint for wider adoption, but urban and suburban corridors are increasingly well-served. Chinese EV manufacturers currently lead in price-competitive electric platforms suitable for expedited delivery. Operators running predictable daily routes should evaluate electric options now, as total cost of ownership is already lower than diesel equivalents in many scenarios.