Technical Support

Cooperative Case

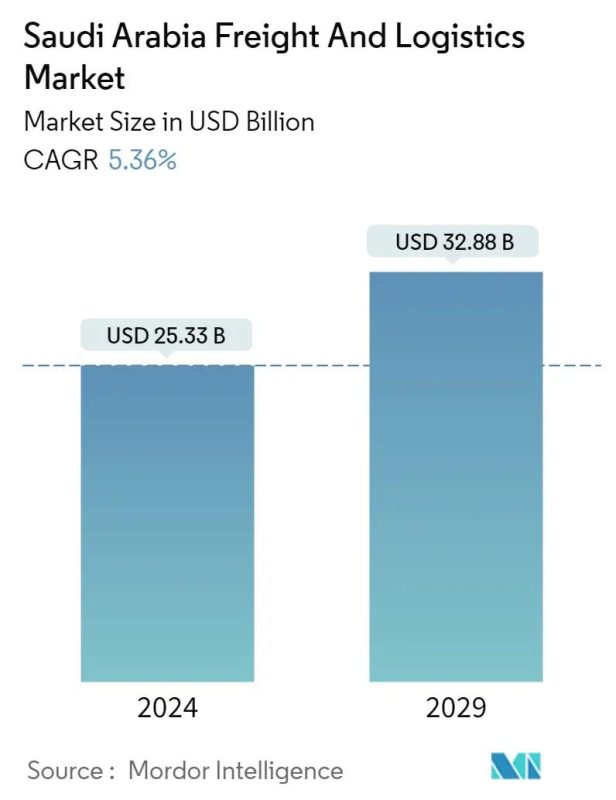

Transforming Freight Transportation in Saudi Arabia: A New Era of Growth

Saudi Arabia’s logistics sector is undergoing a dramatic transformation, driven by ambitious national goals and unprecedented investment in infrastructure. The trucking industry sits at the heart of this evolution, connecting ports, industrial zones, and urban centers across a vast geographic landscape. As the Kingdom diversifies its economy beyond oil, road freight has emerged as a critical enabler of commerce and development.

This article explores the forces reshaping commercial road transport in Saudi Arabia, from advanced technologies and regulatory shifts to workforce strategies and sustainability mandates. Whether you are a fleet operator, logistics professional, or investor, understanding these dynamics is essential for navigating the decade ahead.

Saudi V ision 2030 Logistics and the Road Freight Sector

ision 2030 Logistics and the Road Freight Sector

The Kingdom’s Vision 2030 framework positions logistics as a foundational pillar of economic diversification. The National Transport and Logistics Strategy aims to elevate Saudi Arabia into a top-ten global logistics hub, with road freight carrying approximately 30% of all domestic cargo movement. Government spending on highway expansion, dry ports, and intermodal facilities has exceeded SAR 120 billion since the strategy’s inception.

These investments directly benefit commercial carriers by reducing transit times, lowering vehicle maintenance costs, and opening new trade corridors. The Riyadh–Jeddah expressway upgrades and the Northern Corridor linking NEOM to central distribution hubs exemplify how infrastructure shapes freight demand. For operators considering how to start a trucking company in 2026, the regulatory environment has also become more accessible, with streamlined licensing through the Transport General Authority (TGA).

Key Infrastructure Projects Supporting Road Freight

| Project | Investment (SAR Billion) | Expected Completion | Impact on Freight |

|---|---|---|---|

| Riyadh–Jeddah Expressway Expansion | 25 | 2027 | 40% reduction in cross-country transit time |

| King Salman International Logistics Zone | 18 | 2028 | Integrated multimodal hub near Riyadh |

| Jubail–Dammam Industrial Corridor | 12 | 2026 | Dedicated heavy-vehicle lanes for petrochemical transport |

| NEOM Northern Logistics Gateway | 9 | 2029 | New demand corridor for construction materials |

Technology and Automation Reshaping Fleet Operations

Digital transformation is no longer optional for Saudi carriers. Fleet management technology now encompasses real-time GPS tracking, predictive maintenance algorithms, AI-powered route optimization, and electronic logging devices mandated by TGA. According to a 2025 report by the Saudi Logistics Academy, over 60% of medium-to-large fleet operators have adopted at least one digital platform for dispatch and monitoring.

The conversation around autonomous trucks Middle East has moved from speculation to pilot programs. In early 2026, the Public Investment Fund–backed venture TuSimple Arabia began testing Level 4 autonomous heavy trucks on the Riyadh–Dammam highway under controlled conditions. While full commercial deployment remains years away, platooning technology—where a lead driver guides a convoy of semi-autonomous vehicles—is already reducing fuel consumption by 10–12% in trial runs.

Supply Chain Digitization in Practice

Beyond the vehicle itself, supply chain digitization is connecting shippers, carriers, and receivers through unified platforms. Saudi startups like Trukker and Naqel Express have built freight marketplaces that match available capacity with cargo demand in real time. These platforms reduce empty-mile percentages—a persistent inefficiency that historically wasted 25–30% of total kilometers driven.

Blockchain-based documentation is also gaining traction for cross-border shipments through GCC customs unions. This eliminates days of paperwork delays at border checkpoints, a tangible benefit for operators running international routes. The integration of these tools reflects broader trucking industry technology and automation trends visible across global markets.

Addressing the Driver Workforce Challenge

Like many nations, Saudi Arabia faces a structural shortage of qualified commercial drivers. The TGA estimates a gap of approximately 35,000 heavy-vehicle operators as of early 2026, driven by an aging workforce, demanding working conditions, and competition from other sectors offering comparable wages with better schedules.

The Kingdom’s Saudization policies add complexity. Nitaqat quotas require increasing percentages of Saudi nationals in transport roles, yet cultural perceptions and the physical demands of long-haul routes have limited domestic recruitment. Effective trucking industry driver shortage solutions now combine multiple approaches rather than relying on a single fix.

Workforce Strategies Gaining Traction

- Subsidized training academies: The Saudi Logistics Academy graduated over 4,000 new commercial license holders in 2025, with expanded capacity planned through 2028.

- Improved compensation structures: Leading carriers like SACO Logistics and Almajdouie have introduced performance bonuses, health coverage, and scheduled rest rotations to improve retention.

- Technology-assisted driving: Advanced driver-assistance systems (ADAS) reduce fatigue and make the profession more accessible to a broader demographic, including younger recruits.

- Flexible contract models: Gig-style platforms allow part-time drivers to accept loads on their schedule, expanding the available labor pool without full-time commitments.

Regulatory Landscape and Compliance Updates

Saudi transport regulations have tightened considerably as the sector professionalizes. The TGA’s 2025 regulatory overhaul introduced mandatory electronic logging, stricter hours-of-service limits (maximum 10 hours driving within a 14-hour window), and enhanced vehicle inspection protocols. Carriers operating without compliance face fines starting at SAR 50,000 per violation.

Environmental regulations represent the next frontier. The Saudi Green Initiative has set targets for reducing transport-sector emissions by 30% before 2035. This translates into phased requirements for Euro VI–equivalent engine standards, mandatory emissions reporting for fleets exceeding 20 vehicles, and incentives for LNG and electric vehicle adoption. Understanding trucking industry regulations and compliance updates is now a core operational competency rather than a back-office concern.

Emissions Standards Timeline

| Requirement | Effective Date | Applicable Fleet Size |

|---|---|---|

| Euro VI engine standard for new registrations | January 2027 | All new heavy vehicles |

| Annual emissions reporting | July 2026 | Fleets of 20+ vehicles |

| Carbon offset program participation | January 2028 | Fleets of 50+ vehicles |

| Zero-emission vehicle quota (5%) | January 2030 | Fleets of 100+ vehicles |

Market Trends Shaping the Next Five Years

Several converging forces define trucking industry trends 2026 within the Saudi context. E-commerce growth continues at 20%+ annually, creating demand for last-mile and middle-mile capacity. Mega-projects like NEOM, The Line, and the Red Sea Development generate sustained construction logistics needs through the end of the decade.

Consolidation is accelerating among mid-sized carriers. Operators with fewer than 50 vehicles face mounting pressure from compliance costs, technology investments, and customer expectations for digital visibility. Industry analysts project that the top 20 carriers will control 45% of market revenue by 2028, up from approximately 30% in 2024.

Sustainability as Competitive Advantage

Forward-thinking operators are discovering that green logistics is not merely a compliance burden but a commercial differentiator. Major shippers—particularly multinational manufacturers and retailers—increasingly require carbon-footprint data from their transport partners. Carriers investing in LNG-powered fleets, aerodynamic trailer designs, and route optimization report winning contracts specifically because of their sustainability credentials.

The freight transportation Saudi Arabia market is also seeing early adoption of hydrogen fuel-cell trucks for specific corridors, with ARAMCO-backed pilot programs testing viability on the Yanbu–Jeddah industrial route.

Practical Guidance for Operators and Investors

For those entering or expanding within this sector, success depends on aligning with structural trends rather than competing solely on price. The following principles guide sustainable growth:

- Invest in digital infrastructure first. A transport management system (TMS) and electronic proof-of-delivery are table stakes for winning contracts with major shippers.

- Plan for regulatory escalation. Build compliance costs into five-year financial models. Retrofitting fleets reactively is far more expensive than proactive planning.

- Develop driver value propositions. The carriers that solve recruitment and retention will have structural advantages as demand grows.

- Consider corridor specialization. Rather than competing across all routes, dominating specific trade lanes builds operational expertise and customer loyalty.

For comprehensive logistics consulting and fleet optimization services tailored to the Saudi market, Mettlead offers strategic guidance for operators at every scale.

Frequently Asked Questions

What is driving growth in Saudi Arabia’s road freight sector?

Growth is primarily driven by Vision 2030 infrastructure investments, e-commerce expansion, and mega-project construction logistics. Government spending on highways, dry ports, and intermodal facilities has created new demand corridors while reducing operational costs for carriers serving existing routes.

How is automation affecting commercial transport in the Kingdom?

Automation is progressing in stages. Currently, fleet management technology, AI route optimization, and driver-assistance systems are widely adopted. Autonomous vehicle pilots are underway on select highways, though full commercial deployment without human oversight is not expected before 2030. Platooning technology offers near-term fuel savings of 10–12%.

What qualifications are needed to operate a freight company in Saudi Arabia?

Operators must obtain a commercial transport license from the Transport General Authority, meet Saudization workforce quotas under Nitaqat, maintain vehicles compliant with safety and emissions standards, and implement electronic logging systems. The TGA has streamlined the application process digitally, reducing approval timelines from months to weeks for qualified applicants.

How are environmental regulations changing for Saudi carriers?

The Saudi Green Initiative mandates progressive emissions reductions. New heavy vehicles must meet Euro VI standards from 2027, annual emissions reporting begins for larger fleets in mid-2026, and zero-emission vehicle quotas take effect in 2030. Carriers investing early in cleaner technologies gain both compliance readiness and competitive advantages with environmentally conscious shippers.

Where can operators find strategic support for fleet growth and optimization?

Specialized consultancies provide market entry strategies, fleet planning, regulatory compliance guidance, and technology implementation support. Mettlead’s logistics advisory services help operators align their growth plans with Saudi Arabia’s evolving transport landscape, from route analysis to workforce development strategies.